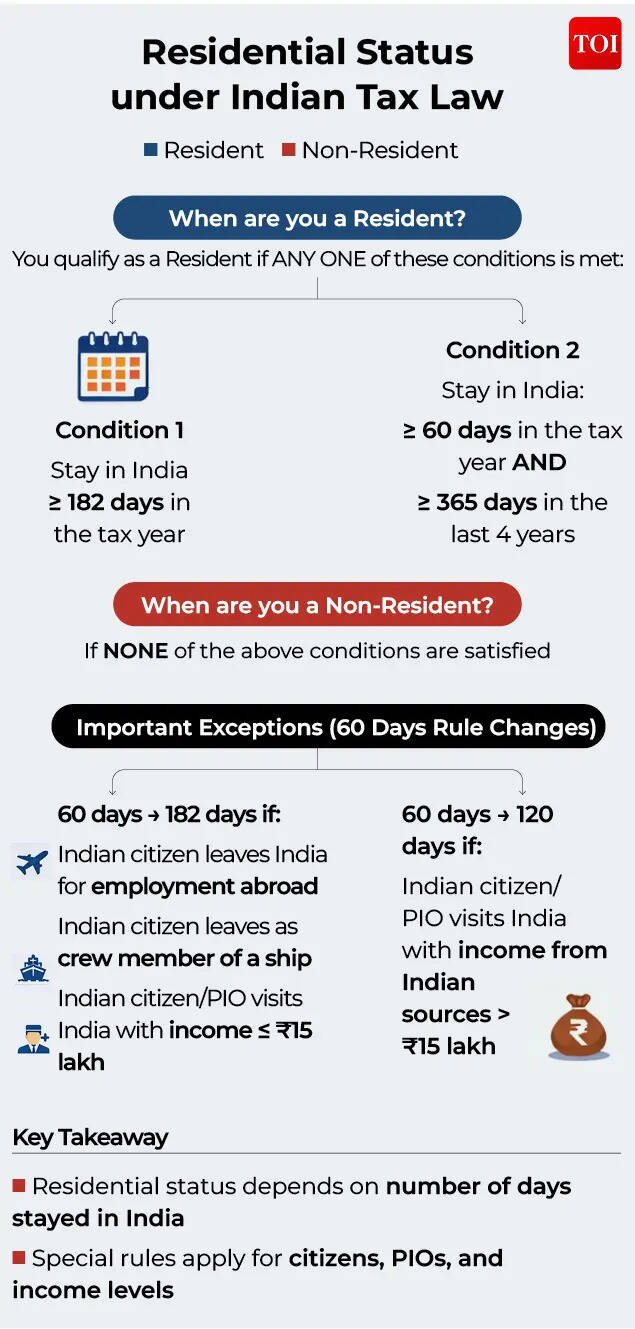

In at the moment’s globalised world, the power to reside in one nation and work in one other nation for an employer in the third nation is changing into a norm somewhat than an exception. Professionals are more and more constructing careers throughout borders as organisations are more and more hiring finest expertise to assist them from wherever. Amid this rising expertise fungibility, the elements that play a important function in figuring out tax legal responsibility relying on one’s nation are residential standing, citizenship, situs of earnings, and many others.. However, figuring out residential standing varies from nation to nation and it may very well be advanced due to numerous doable interpretations.As per Indian tax legal guidelines, the extent to which a person shall be taxed is decided primarily based on their residential standing. We have tried to carry out a complete understanding of India’s residency rules, learn in conjunction with worldwide tax ideas and treaty frameworks for precisely figuring out tax publicity in a cross-border context.How India’s residency rules differ from different nationsIndia determines a person’s tax residency totally on the premise of bodily presence (regardless of the aim of stay) throughout the nation. The variety of days current offers a mechanical framework for classifying taxpayers’ residential standing below Indian tax legal guidelines.In distinction, many developed tax jurisdictions undertake a extra holistic method in figuring out residency. While the variety of days current thresholds proceed to play an essential function globally, nations such because the US, UK, Australia, France and many others. complement bodily presence assessments with a broader analysis of a person’s private and financial connections. These might embrace elements similar to the placement of household, availability of a everlasting residence, place of employment, domicile, and the centre of financial or important pursuits. In sure jurisdictions, further issues, similar to citizenship, additionally affect the dedication of tax residency.As a consequence, in contrast to India’s predominantly bodily presence-primarily based framework, a number of jurisdictions undertake a multi-issue evaluation that balances bodily presence with qualitative elements reflecting the person’s broader private and financial integration throughout the nation. This method is meant to make sure that tax residency aligns extra intently with the person’s actual connection to the jurisdiction somewhat than being decided solely by thresholds of bodily stay.At the worldwide stage, the Organisation for Economic Co-operation and Development (OECD) offers guiding ideas on tax residency by the OECD Model Tax Convention, which serves as the inspiration for a lot of bilateral tax treaties. The OECD framework is especially related in scenario of twin residency in order to allocate residency to a single jurisdiction in a method that displays the person’s closest and most substantive connections by the use of tie-breaker rules primarily based on standards such because the existence of a everlasting residence, the centre of significant pursuits, ordinary abode, and nationality.How to decide residential standing as per Indian tax legal guidelinesThe Residential standing of a person will be categorised into two major classes:An particular person would qualify as a Resident if both (1 or 2) of the next two primary circumstances are happy. If none (1 and a couple of) of the circumstances are happy, then a person could be handled as Non-resident in India:

- He/ she stays in India for 182 days or extra through the related tax yr; (or)

- He/ she stays in India for 60* days or extra through the related tax yr and twelve months or extra in 4 tax years instantly previous the related tax yr.

*60 days talked about in level 2 above ought to be learn as 182 days, if –

- An Indian citizen leaves India for the aim of employment outdoors India in the tax yr;

- An Indian citizen leaves India as a member of the crew of an Indian ship / international sure ship in the tax yr;

- An Indian citizen or a particular person of Indian origin comes on a go to to India in the tax yr and have whole earnings from Indian sources up to Rs 1,500,000 through the related tax yr.

*60 days talked about in level 2 above ought to be learn as 120 days, if –

- An Indian citizen or a particular person of Indian origin comes on a go to to India in the tax yr having whole earnings from Indian sources exceeding Rs 1,500,000 through the related tax yr.

Residents in India may very well be additional categorised as ‘Resident and Ordinarily Resident’ (ROR) or ‘Resident but Not Ordinarily Resident’ (RNOR).

An particular person shall be categorised as ROR if each the next circumstances are happy and as RNOR if both 1 or not one of the following circumstances are happy:

- He/ she qualifies as a Resident (as per primary circumstances) in India in two out of ten tax years instantly previous the related tax yr; and

- He/ she stays in India for 730 days or extra in seven tax years instantly previous the related tax yr.

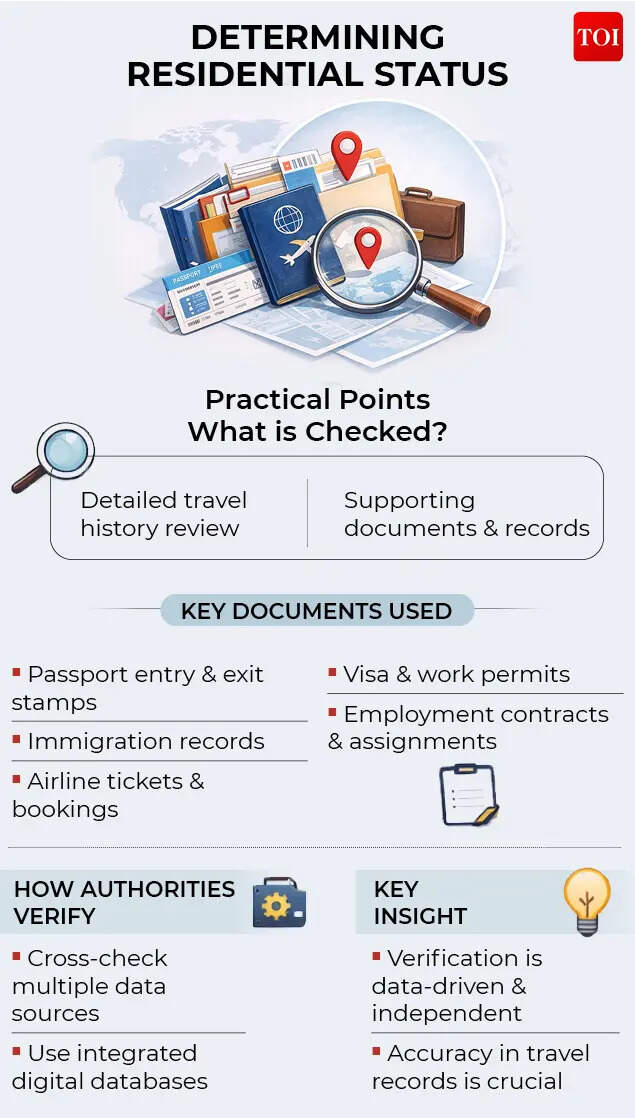

Residential standing should be decided individually for every tax yr, primarily based on a person’s bodily presence in India through the related tax yr. In computing the variety of days in India, each the day of arrival and the day of departure shall be counted as day current in India.Tax publicity primarily based on residential classificationAn particular person qualifying as a ROR is topic to tax in India on their worldwide earnings and non-resident is topic to tax in India on their Indian supply and acquired earnings in India. In distinction, a RNOR is liable to tax solely on earnings that’s earned or acquired in India, or earnings arising from a enterprise managed or a career arrange in India, with most international earnings remaining outdoors the Indian tax internet.The RNOR classification typically serves as a transitional profit, significantly for people returning to India after an prolonged interval of employment abroad, in addition to for international nationals in the preliminary years of their stay in India, earlier than their worldwide earnings turns into totally taxable in India.Illustrative case researchBelow are some sensible illustrations to comprehend how residency rules function in India.Case Study 1: Leaving India to take up an employment overseasX, an Indian citizen employed with ABC Pvt. Ltd., departs from India on 15 July 2025 to take up an employment task in the UK, with the payroll transitioning to ABC Plc UK. During the related tax yr 2025–26, X was current in India from 1 April 2025 to 15 July 2025 and doesn’t return to India for the rest of the yr ending 31 March 2026.Given that X left India for the aim of employment outdoors India, the edge of 182 days applies for figuring out his residential standing. As his whole interval of stay in India through the tax yr is lower than 182 days, X would qualify as a Non-Resident for the tax yr 2025–26.Case Study 2: Leaving India for a brief-time period task and returning again to India in the identical tax yrConsider a situation the place Y departs from India on 1 June 2025 to take up a brief-time period task in Singapore however subsequently returns to India on 14 December 2025. During the related tax yr 2025–26, Y is current in India for 62 days prior to departure (1 April to 01 June 2025) and for a additional 108 days following return (14 December 2025 to 31 March 2026). Accordingly, the entire interval of stay in India through the yr quantities to 170 days.Given that Y initially left India for the aim of employment outdoors India, the 182-day threshold would apply for figuring out residential standing. As the entire stay in India through the tax yr doesn’t exceed 182 days, Y would qualify as a Non-Resident for tax yr 2025-26.Case Study 3: Leaving India for a lengthy-time period task overseas and returning after few yearsConsider a person, Z who relocated to the US on 10 August 2023 for employment (by no means been overseas in the previous) and continues to reside in the US for the following years. Z returns to India for good on 20 January 2026 with the intention of residing completely.During the related tax yr 2025–26, Z is current in India for 71 days (from 20 January 2026 to 31 March 2026). Prior to departing India in August 2023, the person had spent a substantial interval in India, ensuing in an combination presence exceeding twelve months through the 4 tax years previous tax yr 2025–26.In such a situation, though the person’s stay in India through the related tax yr 2025-26 doesn’t exceed 182 days, the person would however qualify as a Resident in India by advantage of satisfying the 60 days plus twelve months situation.Practical issues in figuring out residential standingIn follow, the dedication of residential standing necessitates a detailed overview of a person’s journey historical past and supporting documentation. The Indian tax authorities throughout assessments depend on a number of knowledge factors to confirm the interval of stay in India, together with:

- Passport entry and exit stamps

- Immigration information maintained by authorities

- Airline journey itineraries and reserving historical past

- Visa and work allow documentation

- Employment agreements and task letters and many others.

With the rising digitisation and integration of immigration and journey databases, tax authorities might confirm such data independently.

Some essential watch factorsGlobally cell workforce should have a clear understanding of tax residency rules due to their worldwide journey patterns and abroad assignments.Individuals can keep away from the danger of non-compliance by intently monitoring the variety of days spent in India throughout every tax yr to reassess their residential standing on an annual foundation. As the residential standing might range relying on journey patterns and private circumstances. Particular consideration could also be paid to particular provisions relevant to Indian residents leaving India for employment overseas or visiting India and people returning after lengthy abroad assignments.Individuals ought to successfully apply tie breaker rules in case of doable twin residency below relevant tax treaty provisions.Since India’s residency framework is predicated on bodily days’ presence, subsequently adopting a proactive method by sustaining correct journey information, understanding the relevant authorized provisions, and periodically reviewing one’s residential place might assist guarantee compliance and keep away from any unexpected tax penalties.(Ravi Jain is Tax Partner at Vialto Partners. Vikas Narang, Director and Pawan Digga, Manager at Vialto Partners have additionally contributed to the article. Views are private)